Kenya's Journey Towards a Digital Economy

- Zaara Hajiyani and Roshni Patel

- 1 day ago

- 4 min read

Introduction:

Over the past 2 decades, Kenya has come out as one of Africa’s leading digital economies, supported by rapid technological development. A major milestone in this transformation was the launch of M-pesa in 2007, a mobile money service that allows users to send, receive and manage money through their mobile phones even without a traditional bank account. By increasing access to financial services, M-pesa was able to play an important role in improving financial inclusion across Kenya.

The year 2007 serves as the reference point for this investigation, because it marks the beginning of Kenya’s digital financial revolution. This report analyzes trends in Kenya's GDP, mobile cellular subscriptions, and economic stability indicators to explore the following research question: How has M-Pesa influenced Kenya’s economic growth and transition towards a digital economy since 2007?

Insights and Analysis

The data analyzed in this project shows a clear pattern: Kenya’s economy has experienced significant positive transformation since the introduction of M-Pesa in 2007. The results show a rather rapid growth in the economy.

Figure 1:

which displays Kenya’s GDP over time, shows that the country’s Gross Domestic Product began growing more rapidly after 2005, with a consistent upward trend continuing after M-Pesa’s launch. This is further supported by Graph 3, a bar chart comparing average GDP before and after 2007, which presents a large increase from approximately 6 trillion to 36 trillion Kenyan Shillings.

Figure 3:

Looking at Kenya's GDP in its monetary terms further supports this long term pattern of economic growth. Graph 6 presents Kenya’s Gross Domestic Product in billions of US dollars, showing a significant increase in economic growth after 2007.

Figure 6:

All together, these trends suggest that the digital financial services introduced by M-Pesa coincided with significant economic growth and overall economic activity.

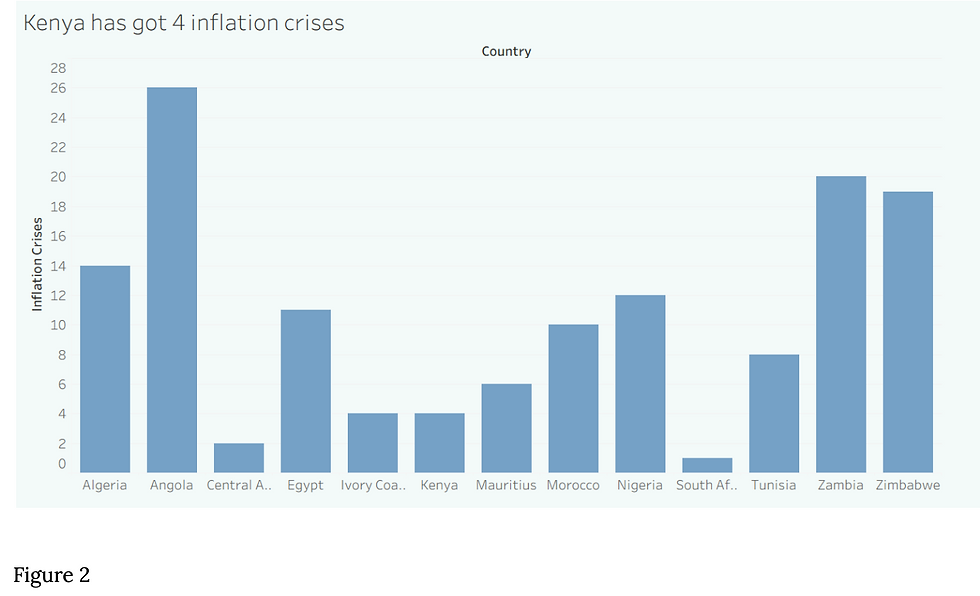

Another key observation is the improvement in economic stability. Graph 2 shows that Kenya experienced only 4 inflation crises, which is relatively low compared to several other African countries.

Figure 2:

Similarly, Graph 4 indicates that currency crises became less frequent after 2007.

Figure 4:

The graph presents that Kenya experienced few currency crises over the recorded period, with most years showing 0,which indicates no crisis. However, crises occurred in 1975, 1979, 1980, 1986, 1989, 1990, 1995, 2000, and 2007, showing they were occasional rather than frequent. Kenya’s probability of experiencing a currency crisis is 13.43%, compared to the overall African probability of 13.22%, making it only 0.21 percentage points higher. This suggests that Kenya’s currency stability is similar to the wider African trend.

The chance of an African country experiencing multiple financial crises in the same year is 7.93% showing that It is uncommon for African countries to face several types of financial crises at the same time. Kenya’s probability of a currency crisis is 13.43%, which is slightly above the overall African average of 12.46%.

Overall, the data suggests that Kenya's economic environment became more stable following the launch of M-Pesa, while this trend cannot really be explained entirely by mobile money, the growth of digital financial services are likely to be contributing to a more accessible financial system.

The rapid growth in mobile connectivity, shown in Graph 5, provides important supporting evidence. Mobile cellular subscriptions per 100 people rose sharply after 2005 and reached over 120 in recent years.

Figure 5:

The graph demonstrates a significant increase in Kenya’s mobile cellular subscriptions across the years. From 1960 to 2000, mobile subscriptions remained at 0 showing growth, but they began rising rapidly after 2001, increasing from 1 subscription per 100 people to 127 per 100 people by 2025. The fastest increase occurred after 2007, following the introduction of M-Pesa, showing a major expansion in mobile access and digital connectivity.

This growth is supported by the increase in mobile subscriptions, which indicates greater access to digital financial services and communication. The rise in mobile usage highlights how mobile technology became an important part of Kenya’s economic development by making financial services more accessible and enabling easier access to services.

This expansion of mobile phone usage created the necessary infrastructure for M-Pesa to reach millions of Kenyans, including those in rural areas who previously had limited access to banking services which explains the trend in graph 6. As a result, financial inclusion improved significantly, allowing more people to participate in the formal economy through easier remittances, payments, and savings.

In my view, these changes happened due to Kenya's pre 2007 economic situation: lack of access to affordable financial services.By providing fast, convenient and low cost methods of transferring money through phones, M-pesa was able to create wider economic contributions amongst individuals and businesses. These small developments lead to expanding Kenya in financial access and increase economic participation across kenya.

Recommendations

To build on this progress, the government should focus on spreading digital infrastructure to underserved areas, promoting digital literacy, and strengthening cybersecurity for mobile money platforms. More investment in technology adoption by businesses will help ensure that Kenya’s digital economy remains strong and inclusive in the future.

In conclusion, the introduction of M-Pesa in 2007 marked a significant turning point in Kenya’s economic journey. The data clearly shows that Kenya’s economy has grown stronger and more stable since the launch of this mobile money service. GDP has increased greatly, mobile phone usage has expanded rapidly, and the frequency of economic crises has reduced. These changes show how digital financial tools can drive financial inclusion for all and support broader economic development.

However,a few challenges remain. Issues like digital divides, cybersecurity risks, and the need for more digital literacy must be addressed to ensure that the benefits of the digital economy reach all citizens.

Overall, Kenya’s journey with M-Pesa serves as a notable example for other developing countries. With continued investment in technology and inclusive policies, Kenya will be able to further strengthen its position as a leader in Africa’s digital economy.